In October 2025, I took part in the Sino-Brazilian Engineers Capacity Building Program Mission in Jinan, China — an initiative promoted by the Brazilian Federation of Engineers Associations (Febrae), supported by the State Grid Corporation of China (SGCC) and the China Society of Engineering (CSN). I visited solar panel factories, electric vehicle plants, and delved into technologies redefining global construction and energy. The experience was recognized by Business magazine in its December 2025 edition. Now, five months later, with the Middle East aflame and oil breaking records, everything I saw there has gained an urgency no one expected. This article aims to put the two worlds into perspective.

What is happening: facts, figures, and the voice of the IEA

On Monday, March 23, 2026, the Executive Director of the International Energy Agency (IEA), Fatih Birol, made a statement leaving no room for interpretation: the current energy crisis is worse than the two consecutive oil crises of the 1970s — the 1973 embargo when Arab countries removed 10 million barrels per day from the market, and the 1979 crisis triggered by the Iranian Revolution.

| Indicator | Number |

|---|---|

| Barrels/day through the Strait of Hormuz (normal) | 20 million — 20% of global oil |

| Peak Brent crude price per barrel | US$126 — highest in 4 years |

| Severely damaged energy assets | 44 in 9 countries |

| Barrels released from strategic reserves (IEA) | 400 million — equivalent to only 20 days of normal flow |

The conflict between the US, Israel, and Iran, starting February 28, 2026, led to the effective closure of the Strait of Hormuz by Iran beginning March 4. The 34 km wide passage at its narrowest point is the only maritime outlet for oil production from Saudi Arabia, Kuwait, Iraq, the United Arab Emirates, and Iran itself.

"The single most important solution to this problem is reopening trade through the Strait of Hormuz. Our reserves will help ease the pain, but this is not the solution — it is only temporary relief."

Fatih Birol — Executive Director, IEA — Canberra, 03/23/2026

To understand the scale of the collapse: the IEA released 400 million barrels from global strategic reserves — a historic volume. But global consumption is 105 million barrels per day. This means the entire release covers less than four days of global consumption. Even compared to the normal flow through Hormuz, it only represents 20 days of replenishment. The structural problem remains untouched.

The cascade effect beyond oil

Birol emphasized that the problem goes far beyond the barrel of oil. The "vital arteries" of the global economy disrupted include petrochemicals, fertilizers, sulfur, and helium — inputs embedded in agriculture, the semiconductor industry, and even healthcare.

⚠️ Attention, agricultural sector: The blockade affected up to 70% of the Gulf countries' food imports, which rely on the Strait for more than 80% of their calorie intake. The regional food crisis is already underway, with prices rising between 40% and 120% in local supermarkets.

Asian financial markets collapsed in the early hours of Monday: Japan's Nikkei 225 fell 3.5%, South Korea's Kospi plunged 4.9%, and Hong Kong's Hang Seng retreated 2.7%. Japan, which imports around 70% of its oil via the Strait, has already announced the release of 80 million barrels from its national reserves.

Why this crisis is different from those in the 1970s — and why it matters

In the 1970s, humanity was caught completely off guard. There was no alternative to oil for mobility, power generation, or heating. The entire world depended on a single source, from a single region, transported via a single route.

In 2026, the geopolitical situation is equally severe — or worse, as the IEA points out. But the technological context is radically different. This is exactly what I saw firsthand in China.

| Dimension | 1970s Crisis | 2026 Crisis |

|---|---|---|

| Energy alternatives | Virtually none | Solar, wind, nuclear, EVs at industrial scale |

| Solar energy cost | Commercially nonexistent technology | 90% cost drop in 10 years |

| Electric vehicles | Experimental concept | Nearly 48% of global sales in 2026 (China) |

| Strategic reserves | Nascent or nonexistent | 4.1 billion barrels globally (~120–180 days) |

| Alternative routes | Extremely limited | Partial: Saudi and Emirati pipelines (3.5–5.5M bpd) |

| Response speed | Months for any adjustment | Days to mobilize technology and multilateral coordination |

The fundamental difference is this: in the 1970s, the only recourse was political pressure and rationing. In 2026, for the first time in history, there is a real technological way out — and it is being manufactured at industrial scale in factories I visited in October 2025.

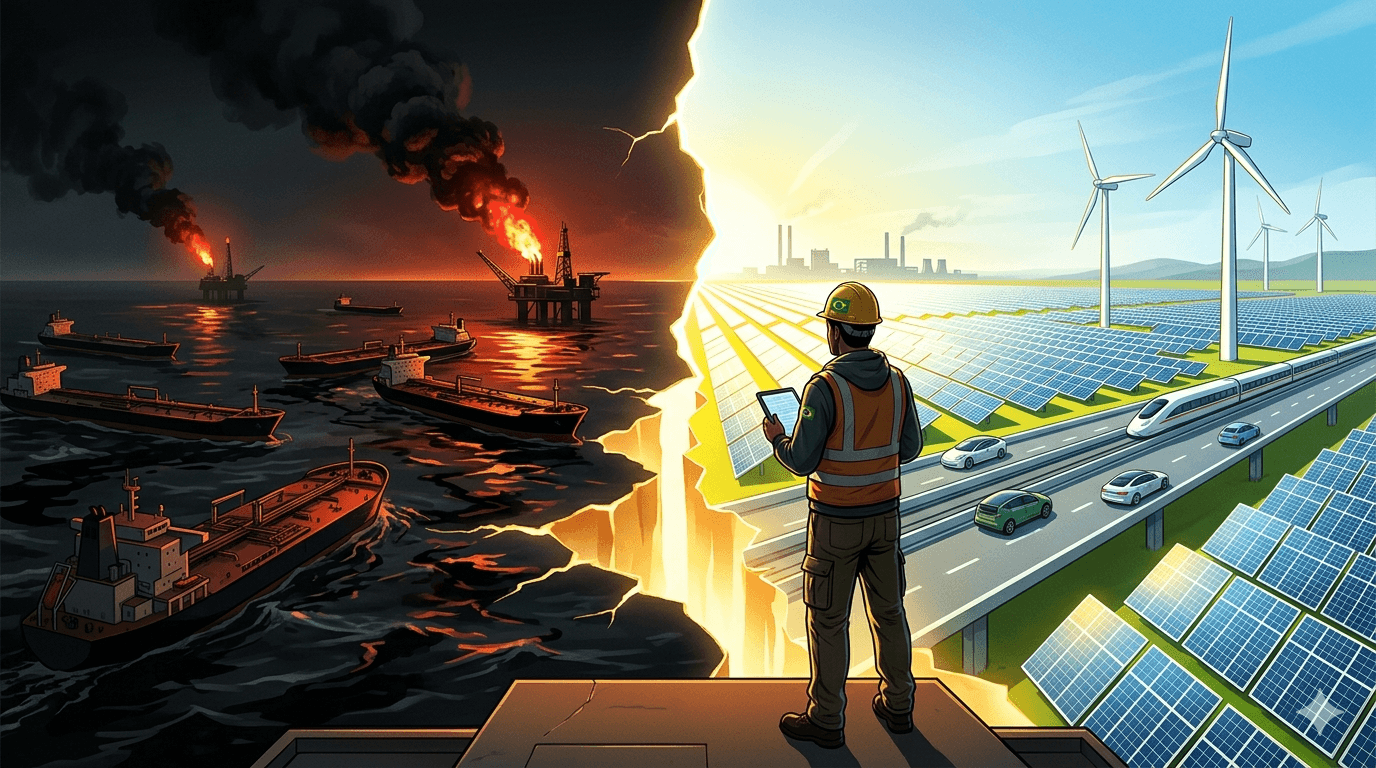

What I saw in China: where crisis and opportunity meet

The trip to China in October 2025 was not tourism. It was a technical and institutional exchange mission — and what I found there explains why, even with the world aflame in the Middle East, part of the global industry looks East with hope — not fear.

Solar dominance: 80% of global capacity in a single country

China controls approximately 80% of global solar panel manufacturing capacity. In a single year, the country produced 588 GW of panels — nearly double the world demand during that period. This overproduction, once seen as a market problem, now appears in a different light: a technological reserve available to the world.

| Indicator | Number |

|---|---|

| Global solar manufacturing capacity | 80% located in China |

| Lithium-ion battery supply chain | 65% is Chinese |

| Solar panels produced in one year | 588 GW — nearly 2x world demand |

| EV exports from China (2024) | US$ 46 billion |

The cost of a solar panel has dropped over 90% in the last fifteen years. The factories I visited operate at volumes incomprehensible to any Western industrialist: automated production lines, storage batteries stacked in warehouses the size of neighborhoods, and electric vehicles rolling off lines with costs that compete with — and often outperform — traditional combustion cars.

Electric vehicles: China as the new OPEC of mobility

Brands like BYD, Chery, Geely, and Changan already export nearly 6 million electric vehicles per year — more than any other country. The Chinese government plans that nearly half of all vehicles sold will be electric or plug-in hybrids by the end of 2026, targeting 32.3 million units in the global market.

For Brazil, this is not an abstract threat: it is a concrete opportunity to access technology that would previously be unreachable. With oil at US$126 per barrel and a prospect of a prolonged crisis, the opportunity cost of not accelerating the electrification of the national fleet has never been higher.

"Two-thirds of China's clean technology capacity will be surplus to domestic needs by 2030. This surplus will find a market somewhere. The question is: will it be here in Brazil, or will we let this window pass?"

Felipe Antonio Xavier Andrade · Redax Engenharia · technical exchange in China, October 2025

What Tesla and major players already see

While the world debates the crisis, strategic players are already acting. Tesla is negotiating the purchase of US$ 2.9 billion in solar manufacturing equipment from Chinese suppliers to install 100 GW of solar capacity in the US by 2028. Even with American tariffs, Chinese technology is so competitive that it offsets the additional cost. China, in turn, plans US$ 94 trillion (G20 projection) in global clean energy infrastructure by 2040 — and already holds clean energy production equivalent to Brazil's entire GDP.

What this means for Brazil — and Redax

Brazil holds a unique position on this board. We are one of the most privileged countries on the planet for renewable energy resources: among the highest solar irradiation in the world, hydroelectricity, wind, ethanol. Yet at the same time, we have an aging vehicle fleet, an electric matrix that still includes oil and gas thermal plants, and a construction industry beginning to understand the role of energy efficiency as a competitive differentiator.

Immediate risk: inflation of inputs and fuels

With Brent crude oil at US$103–126 per barrel, passing on costs to fuels in Brazil is a matter of time and economic policy. More expensive diesel means more expensive construction — logistics, equipment, materials transport. For the engineering and construction sector, the impact is direct: increased costs for machinery, concrete (whose transport is diesel-intensive), asphalt, and petroleum-derived plastics.

⚠️ Alert for project managers: Projects with 12 to 24-month schedules must immediately review their input budgets. The baseline oil price scenario until September 2026, even with conflict de-escalation, is US$90–110 per barrel. Consider this in your ongoing feasibility studies.

Strategic opportunity: where Redax can act

At the same time, the crisis opens three concrete fronts of opportunity for well-positioned engineering companies:

1. Energy efficiency projects in buildings. With energy more expensive and uncertain, commercial and industrial property owners will accelerate investments in thermal insulation, building automation, and HVAC system efficiency. Redax already operates in this spectrum and can expand its technical offering in this direction.

2. Installation of photovoltaic systems in new and retrofit projects. Brazil has privileged solar irradiation. With increasingly accessible Chinese panels (even with eventual tariffs, competitiveness is structural), the solar cost for end clients has never added up better than it will in the next 18 months.

3. Infrastructure for electric mobility. Condominiums, industrial warehouses, offices, and fuel stations will need electrical adaptations for EV chargers. This is a specialized technical installation market still forming in Brazil — growing regardless of geopolitical scenarios.

Conclusion: crises reveal the future

I left China in October 2025 with a conviction that today's data confirms: the energy problem of 2026 is real, serious, and will be costly for those unprepared. But unlike 1973 or 1979, humanity this time is not empty-handed.

We have solar panels at historically low prices. We have batteries with energy density and durability that would have been science fiction ten years ago. We have electric vehicles competing on equal footing with combustion engines. And in Brazil, we have one of the best natural resources on the planet to make all this work.

The Strait of Hormuz crisis will not end tomorrow. President Trump gave Iran a 48-hour ultimatum — which responded with "if you attack electricity, we will attack electricity." The escalating rhetoric and military tensions should keep markets volatile for weeks or months.

But crises reveal the future. The ’70s accelerated the creation of strategic oil reserves. The 2022 Russia crisis accelerated European energy autonomy. The 2026 crisis will accelerate the transition to distributed, renewable, local energy — worldwide.

The question for us, engineers and construction managers, is simple: will we watch this future happen, or will we build it?

About the author

Felipe Antonio Xavier Andrade is an engineer at Redax Engenharia, headquartered in Osasco, SP. Specialist in engineering applied to the real estate and industrial market. He participated in October 2025 in the Sino-Brazilian Engineers Capacity Building Program Mission (Febrae / SGCC) in Jinan, China, focusing on vehicle electrification and solar energy — an experience featured in Business magazine (Dec 2025).

Sources: CNN International (live updates 03/23/2026), International Energy Agency (IEA), Wikipedia — 2026 Strait of Hormuz Crisis, Wikipedia — Economic Impact of the 2026 Iran War, Al Jazeera, CNBC, NPR, Bruegel Institute, EIA, CNN Brazil, Política Por Inteiro.